UK banks could soon embrace Buy Now Pay Later

loading...

The popularity of Buy Now Pay Later (BNPL) has attracted the attention of the UK’s banks, as transactions are set to surge 60 to 70 percent per year.

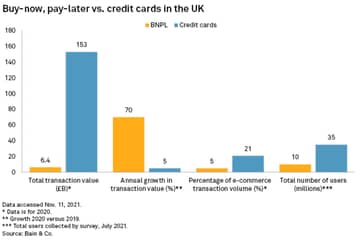

With regulations easing, banks that allow customers the option to pay for goods using interest-free credit will further increase the sector, which currently accounts for 5 percent of e-commerce transaction values according to Bain & Co.

The UK government announced plans to regulate the sector, amid concerns that consumers using BNPL could be racking up substantial debts with multiple companies and facing debt collectors in some cases. The Treasury will consider what kind of regulation is most appropriatefollowing a consultation due to end in January 2022. BNPL falls outside much of the consumer credit protection regime, and banks have thus far been wary of entering the unregulated lending market with its associated reputational risks.

Banks including Barclays, Revolut and Monzo have shown interest, with some already offering similar services.

With banks entering the space, there will be more competition amongst payment services, which to date has been largely occupied by providers including Klarna, Afterpay, Affirm and Paypal. Vogue Business reported BNPL providers “are in various stages of integrating direct shopping into their apps so that users can buy from multiple merchants in one place. Fashion will play a key role in reaching that goal. Still, an all-in-one shopping app isn’t an original endeavor. Google, Facebook, Shopify and many others are also vying for that designation — Amazon.”

Figures from Forrester show 69 per cent of US fashion retailers offer a form of BNPL. When consumers are aware of them, instalment payments usage is high.

The service is well liked by UK consumers, too, who prefer it to credit cards and overdrafts, according to Bain. Its interest-free nature is a big draw, and users in the saved 103 million pounds in credit card interest costs in 2020, Bain estimated.

Article source: S&P Global, Bain & Co.